Retirement Planning

Episode #11 of the course Personal finance concepts by Maureen McGuinness

“Retirement can be a great joy if you can figure out how to spend time without spending money.” –Anon

To most 20-somethings (and even 30-somethings), retirement can feel like a lifetime away. It’s easy to believe that retirement is something that you can take care of when you’re “older,” but when is the right time to start planning for your retirement?

Today.

With goals to buy a house, get married, and have kids, it’s tempting to delay saving for retirement, but taking action today is essential. Why? Because once you set up a system today, your retirement pot grows in the background while you continue with everyday life.

Here are some statistics about retirement from the National Institute of Retirement Security:

• The average American working household has virtually no retirement savings

• Women are 80% more likely than men to be impoverished at age 65

• 62 percent of working households aged 55-64 have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement

How Much is Enough?

Step 1. Calculate how many years you have left until retirement age (you can use 65 as a default).

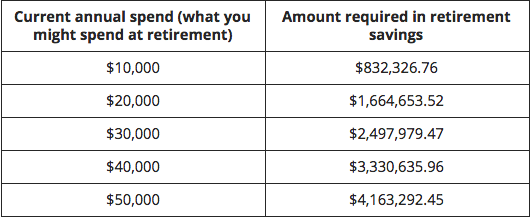

Step 2. One of the biggest worries is that you will run out of money during retirement. Work out how much you spend every year. Use the 4% safe withdrawal rate to figure out how much you need to have saved up by retirement. Assumptions: inflation is around 3%, you retire at 65, and you live for another 25 years.

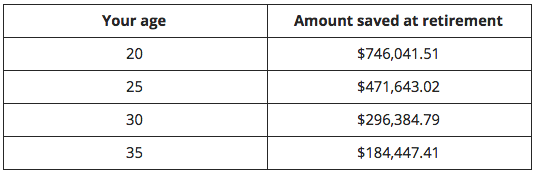

Step 3. Assuming an annual return of around 9%, identify how much you would have at retirement if you contributed $100 a month from today until you retire. Consult the table below:

How to Open a Retirement Account

There are two main ways that you can save for retirement. You can use both if you’re employed by a company but only the latter if self-employed.

401(k) or Company Pension. If you are an employee, your company may offer a 401(k) as a benefit. A 401(k) allows you to contribute your salary before tax to your retirement savings. Some companies offer a matching option whereby they match your contributions up to a certain percentage of your income. You may not always get the money paid to you instead of your 401(k), so if you turn down the matching option, you are turning down free money. Even if they do pay you instead of your 401(k), if you opt out of contributing to your pension, you’ll only get the extra income after it has been taxed.

Individual Retirement Account (IRA) or Self Invested Personal Pension (SIPP). If you are self-employed or your employer does not offer a 401(k), you have the option of setting up your own retirement account via an IRA (in the US) or a SIPP (in the UK). Both products offer tax advantages to help you maximize your savings for retirement.

Roth IRA. When you contribute to a Roth Individual Retirement Account, you pay tax on your contributions but all future withdrawals are tax-free.

Traditional IRA. When you contribute to a Traditional Individual Retirement Account, you do not pay tax on your contributions but all withdrawals are taxed at ordinary income tax rates.

SIPP. In the UK, you can use a SIPP to save for retirement in addition to or as an alternative to a company pension. A SIPP offers up to 45% tax relief on contributions and there is no UK capital gains tax or UK income tax to pay. The tax benefits will depend on your individual circumstances, and tax rules are subject to change by the government.

In summary, start saving for your retirement today.

Recommended book

Share with friends