Introduction to Macroeconomic Theory

Episode #1 of the course Introduction to macroeconomics by Doha Soliman, CFA

Welcome to the course! My name is Doha, and over the next ten days, I’ll guide you through the most important concepts of macroeconomics. We will discuss economic systems such as marxism, capitalism, and socialism. You’ll learn about pioneers of economics, business cycles, economic growth, and game theory. We’ll also explore monetary and fiscal policies, taxation policies, and finish the course off by an overview of global trade.

Today, we’ll start our journey by understanding how economies operate and cover technical terms that will help you grasp the concepts economists use on a regular basis.

Economics, often referred to as the dismal science, is a social science that seeks to explain the means of production, consumption, and distribution within a society, while macroeconomics is a subset of this science that evaluates the aggregate means within an economy. Simply put: While microeconomics concerns itself with how a company operates and the ideal price for a product, macroeconomics is more concerned with all the forces within a country or region and why they behave a certain way.

Economists dedicate their lives to evaluating financial markets, political factors, and consumer behaviors to understand why economies prosper or stagnate. They work hand in hand with politicians, governments, central banks, and corporations with one shared goal: economic growth. Economic growth can be measured in several ways and will be discussed in detail throughout this course. It is important to keep this goal in mind when evaluating any economic theory.

Let’s discuss a few important terms.

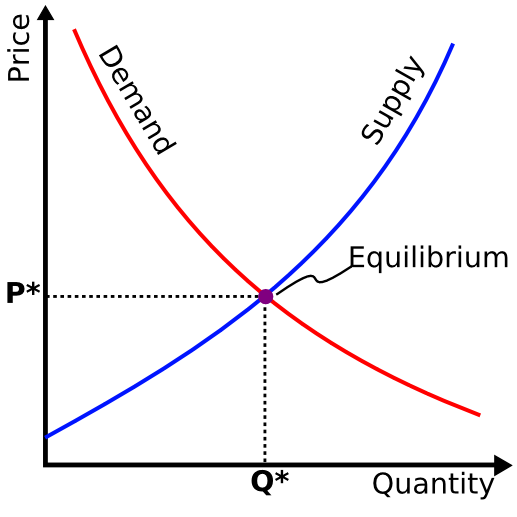

Supply and demand: Many theories of economics, both micro and macro, refer to the laws of supply and demand. Simply put, demand refers to the quantity of a good or service requested by a group of people, whereas supply specifies how much of said good or service is available. For example, you’re in a car dealership with three other buyers looking at cars. There is only one car available in this case. Supply is less than demand, and the car dealer can charge a higher price. As supply and demand meet in a graph, it is called an equilibrium point. In our example, this would mean four cars for four buyers. This equilibrium is a stable price point for outputs and inputs. We will refer to this concept several times throughout our course.

Globalization: This phenomenon relates to the increasing collaboration between nations and the breakdown of barriers throughout the globe. It has resulted in increased mobility, increased trade, and less segregation across countries. For instance, in the past, if I was looking to buy a book, I was limited to what my local bookstore had to offer; now a quick online search gives me access to all the books published worldwide, in any language, genre, or topic I want. This is a perfect depiction of globalization.

Public vs. private sector: The public sector in economics relates to all governments and central authorities, whereas the private sector includes both corporations and private consumers.

Monopoly and oligopoly: A monopoly is an industry in which there is one dominant corporation with no competition. This can be due to barriers to entry, whether financial, structural, or governmental.

An oligopoly is an industry that has a handful of corporations and very little competition among the key players.

We have a lot to cover, so get some rest, and I’ll see you tomorrow. We’ll discuss the schools of thought that have shaped modern-day economic theory.

Recommended book

The Lexus and the Olive Tree: Understanding Globalization by Thomas L. Friedman

Share with friends